When it comes to SBA 504 Loans, what is the Growth Corp difference? While all Certified Development Companies have the same general mission, there are key differences you should be aware of. These differences can make a huge difference in your overall experience during the 504 Loan process.

When it comes to SBA 504 Loans, what is the Growth Corp difference? While all Certified Development Companies have the same general mission, there are key differences you should be aware of. These differences can make a huge difference in your overall experience during the 504 Loan process.

Those who have investigated the U.S. Small Business Administration’s (SBA) 504 financing options have probably seen a reference to a Certified Development Company (CDC), but they may not be fully aware of what a CDC is or what role they play in the SBA 504 Loan process.

What is a Certified Development Company?

According to SBA, “A Certified Development Company (CDC) is a nonprofit organization that promotes economic development within its community through 504 loans. CDCs are certified and regulated by the SBA, and work with SBA and participating lenders (typically banks) to provide financing to small businesses, which in turn accomplishes the goal of community economic development.”

Certified Development Companies are also sometimes referred to as mission-based lenders. There are over 200 CDCs around the country, each with a specific regional focus. Growth Corp is a Certified Development Company authorized to operate in all counties of Illinois, along with small portions of Missouri, Iowa, Indiana, and Kentucky.

What Makes A Certified Development Company a “Mission-Based Lender”?

Perhaps the most important aspect of CDCs is how tightly woven they are with the wider community, specifically the state in which they operate, and even the region surrounding the state in which they are headquartered. CDCs are designed to help strengthen local businesses by connecting them with quality financing for fixed asset investments (real estate or equipment), which, in turn, supports local economies, revitalizes neighborhoods, and breathes new life into local communities.

CDCs are designed to help strengthen local businesses by connecting them with quality financing for fixed asset investments (real estate or equipment), which, in turn, supports local economies, revitalizes neighborhoods, and breathes new life into local communities.

In addition to their focus on building and improving local economies and making it possible for small businesses to thrive, CDCs also focus on achieving specific public policy goals. For instance, they ensure that women and minority business owners are supported, while also providing help for veterans, and even offering advice and guidance for business owners. CDCs are home to experts who have vast knowledge of the local economy and business environment, as well as the resources available to business owners.

What is the Growth Corp Difference?

We may be the largest 504 Lender in Illinois, an Accredited Lender with SBA, and a national leader in volume and quality, but we’re still just a small, focused team working together every day to make the 504 process as smooth as it can be. Let’s break down some questions you should consider when choosing a CDC, with some further details about the Growth Corp difference:

Experience and Staff Longevity

How knowledgeable is the CDC in terms of structuring SBA 504 Loans? Is their focus on the 504 Loan Program or do they offer a wide array of financing programs? Does the CDC have staff dedicated to ensuring your loan not only gets approved, but also gets closed and serviced properly?

At Growth Corp, we know that when it comes to 504 loans, it’s about much more than just getting an approval. It’s the ease-of-mind that comes from knowing Growth Corp’s team has their finger on the pulse of the process from application to funding and even beyond into long-term servicing. It’s knowing you will be informed every step of the way by the point-person responsible for overseeing the closing of your loan. It’s knowing that, given Growth Corp’s extremely low turn-over, you’ll have the same experienced team members continuing to serve you year-after-year. It’s knowing that Growth Corp has one of the highest first-pass approval rates in the country. What does that mean for you? It means your application is structured correctly and accurately before it’s sent to SBA. This facilitates a quicker approval, a more reliable timeframe, and a more efficient process overall.

has their finger on the pulse of the process from application to funding and even beyond into long-term servicing. It’s knowing you will be informed every step of the way by the point-person responsible for overseeing the closing of your loan. It’s knowing that, given Growth Corp’s extremely low turn-over, you’ll have the same experienced team members continuing to serve you year-after-year. It’s knowing that Growth Corp has one of the highest first-pass approval rates in the country. What does that mean for you? It means your application is structured correctly and accurately before it’s sent to SBA. This facilitates a quicker approval, a more reliable timeframe, and a more efficient process overall.

Accreditation with SBA

How many years has the CDC been making SBA 504 Loans? Does the CDC have experience with various industries and business types? Has the CDC worked with a business of your size before? Is the CDC an Accredited Lender (ALP) with SBA? What are the CDCs first-pass approval rates for application packages submitted to SBA’s processing center?

Growth Corp has been focused on SBA 504 Loans for 35 years. Since 1988, we’ve proudly helped thousands of businesses facilitate expansion. In fact, our existing portfolio is over $900 million…particularly impressive considering every dollar is tied to a small business in the Midwest. We know small business. It’s our passion. As the largest 504 Lender in Illinois, we have dedicated ourselves to making the 504 Loan Program as efficient and seamless as possible. In fact, Growth Corp has long held Accredited Lender status with SBA. This means, after a thorough review of our policies, procedures, and prior performance, SBA granted us increased authority to process and close 504 loans, which results in an expedited process for both our borrowers and our lending partners.

Accreditation with SBA, accuracy, and quick turn-around times are just some of the reasons why Growth Corp is a national leader for quality and service.

Responsiveness and Reputation

Does the CDC respond in a timely fashion to both small business borrowers and banking partners? Will there continue to be a point-person at the CDC you can call long after your loan is approved? Is the CDC diligent in dealing with SBA on behalf of your loan application?

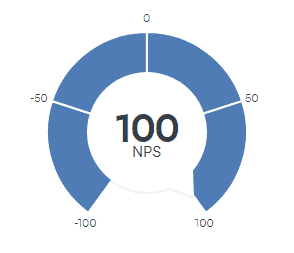

It goes without saying that everyone prefers to work with people who respond in a timely, respectful fashion. Not only that, but with answers that are informative and specific to your project. Recent survey results show Growth Corp has an extremely high satisfaction rating in terms of service and responsiveness, and a 100% Net Promoter Score. Lending partners and small business clients alike have found us to be reputable and will respond in a timely, respectful manner. Your experience with us, and overall experience with the SBA 504 Loan Program, are our highest priority.

It goes without saying that everyone prefers to work with people who respond in a timely, respectful fashion. Not only that, but with answers that are informative and specific to your project. Recent survey results show Growth Corp has an extremely high satisfaction rating in terms of service and responsiveness, and a 100% Net Promoter Score. Lending partners and small business clients alike have found us to be reputable and will respond in a timely, respectful manner. Your experience with us, and overall experience with the SBA 504 Loan Program, are our highest priority.

Relationships with Banks

Does the CDC have a track record of successful partnerships with the banks in your area? Do the banks trust the CDC and its reputation?

During the 35 years Growth Corp has been serving the Midwest, we’ve had the pleasure of working with hundreds of local banks…from Chicago to Carbondale, St. Louis to DeKalb, and everything in between. We’re honored to be trusted by our lending partners and strive to maintain the level of service they have come to expect.

A Footprint in the Community

Does the CDC have good relationships with local banks and businesses? Is the CDCs reputation and credibility sound? Are they investing in the helping to grow the local community?

Perhaps the most important aspect of Growth Corp is how tightly woven we are with the wider community. Growth Corp serves as the “boots on the ground” helping to strengthen local businesses by connecting them with quality financing for fixed asset investments (real estate or equipment), which, in turn, supports local economies, revitalizes neighborhoods, and breathes new life into local communities. In fact, here are just some of the ways communities benefit from our SBA 504 Loan Program:

- Job creation and retention

- Local economic growth & reinvestment

- Encourages free competitive enterprise

- Helps maintain local consumer spending

- Increases consumer confidence

- Supports the development of minority, women and veteran-owned businesses

- Revitalizes business districts

- Expands capital access in economically disadvantaged rural areas

- Encourages innovation

- Growth Corp hosts the Illinois Small Business Development Center for Central Illinois, which helps to ensure that aspiring business owners and growing entrepreneurs have access to business advising and programs at no cost.

Remember, Growth Corp works in conjunction (not in competition) with local banks to offer financing through the SBA 504 Loan Program. Growth Corp packages and processes loan applications through the SBA, and then closes and services those loans once they’ve been approved, making the process much easier for banks. Small business borrowers also gain expert advice from our team on SBA 504 loan terms, rates, uses, and structures. These recommendations are all incredibly beneficial to small businesses that are looking to finance their company’s growth and expansion.

The Role of a Certified Development Company in SBA 504 Lending

Certified Development Companies work in conjunction (not in competition) with local banks to offer financing through the SBA 504 Loan Program. CDCs package and process loan applications through the SBA, and then close and service those loans once they’ve been approved. Small business borrowers gain expert advice from the CDC on SBA 504 Loan terms, rates, uses, and structures. These recommendations are all incredibly beneficial to small businesses that are looking to finance their company’s growth and expansion.

Certified Development Companies work in conjunction (not in competition) with local banks to offer financing through the SBA 504 Loan Program.

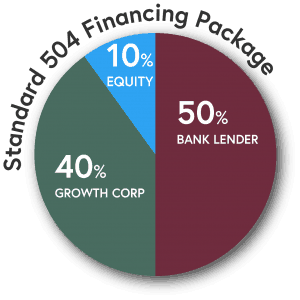

The 504 allows you to keep more of your working capital than most any other commercial loans on the market. Through this loan program, your local lender offers 50% of the financing with favorable terms; 40% of the project costs are financed with a fixed-rate debenture secured with a junior lien (second mortgage) from a Certified Development Company, such as Growth Corp, and backed by a 100 percent SBA guaranty. The borrower contributes a low 10% down payment, which is one of the big attractions of this program.

What are the benefits of SBA 504 Loans for small businesses?

Overall, the most useful benefit of a SBA 504 loan program offers is that the loan offers small business borrowers with quality, long-term, affordable financing while requiring a minimal down payment. Specifically, major benefits of SBA 504 loans include:

- 90% financing (in most cases)

- Longer loan amortizations and no balloon payments

- Low, fixed-rate interest rates (currently below market)

- Minimal down payment

What are the benefits of SBA 504 Loans for lending partners?

- Banks reduces their risk to 50%

- Banks gets first lien position on a 504 loan structure

- When clients are struggling with pending balloons, Growth Corp’s 504 offers refinancing options

- Banks can offer their clients a low, fixed rate product with a long loan term

- SBA lending helps Banks fulfill CRA, Rural and Public Policy goals

- Manages commercial real estate concentration issues

- Opens up lending availability

- Maximizes middle market lending

- High size limits and business size caps

- Preserves working capital, which keeps cash in deposit accounts

- Unique marketing opportunity

- Finances heavy machinery and equipment

- Attracts new business borrowers

How can SBA 504 Loans be used?

SBA 504 business loan must be used for fixed assets (and certain soft costs) including:

- Purchasing existing buildings

- Purchasing land and land improvements such as grading, street improvements, utilities, parking lots and landscaping

- Constructing new facilities or modernizing, renovating, or converting existing facilities

- Purchasing long-term machinery

- Refinancing existing commercial real estate debt

How can a small business become eligible for SBA 504 financing?

To be eligible for the SBA 504 loan program, a small business must operate as a for-profit business and fall within the size standards set by SBA, which is a tangible net worth under $20 million and an average net income of $6.5 million or less after federal income taxes for the preceding two years prior to application. And the business must be purchasing owner-occupied commercial real estate or long-term equipment or machinery.

About Growth Corp

Small Business Growth Corporation (Growth Corp) is a nonprofit, mission-based lender dedicated exclusively to connecting small businesses with quality expansion capital through administration of the SBA 504 Loan Program. With a commitment to economic development, job creation and the small business sector, Growth Corp is ranked a Top 10 National CDC for SBA 504 loan volume and is Illinois’ largest 504 loan provider. In fact, Growth Corp’s substantial portfolio ($880+ million) is particularly impressive because every dollar was utilized by Midwest entrepreneurs to open and expand their small businesses. Contact any member of our lending team today!