Curious as to whether you and your business are a good candidate for an SBA Loan? You’re not alone!

Thousands of businesses, of all shapes and sizes, use SBA 504 loans every year to expand their business. Whether that be buying new equipment, purchasing a new building, constructing a new facility or renovating an existing building. SBA 504 loans are not just for small businesses. Nor are they just for big business. The program is flexible and designed to accommodate businesses in every stage of growth.

Most small businesses qualify for the 504 Loan Program. The business must:

- Be operating a for-profit business

- Be organized as a corporation, sole proprietorship, partnership, LLC, etc.

- Be located in the U.S.

- Have a tangible net worth of less than $15 million and profit after taxes of less than $5 million (including affiliates)

- Have a successful track record and growth potential

- Occupy majority of project property (or owner-occupied property)

Let’s take a look at some of the common questions we hear about qualifying for an SBA 504 Loan.

Is There an Ideal Project Size?

Project sizes typically fall between $250,000 and $10 million, with an average loan size of about $1.5 million.

What Type of Borrower is a Good Candidate for an SBA Loan?

Well, essentially, the big national chains don’t need us. However, just about any other for-profit business owner who wants to build, buy, or improve a commercial property, purchase long-term equipment or refinance commercial mortgage debt will probably be a good fit. Here are some examples…

Medical/Professional

Whether you’re just opening your own practice, or are ready to open a second, third or even tenth office, we’re here to help. We’ve worked with thousands of professionals just like you and we understand the expenses that go into purchasing and furnishing high-end professional offices. Many different types of professionals utilize the 504, such as:

- Doctor’s Offices

- Veterinarian Offices

- Dentists

- Attorneys

- Accountants

- Chiropractors

- Architects

- Graphic Designers

- Physical Therapists

Service Providers

From small, specialty stores to state-of-the-art health clubs, we’ve worked with them all and we understand the nuances and cyclical nature of the service and retail industry. Your number one focus is on your customers and you don’t have time for a lot of paperwork. We get it. That’s why we’ve handled the process for thousands of service providers, such as:

- Restaurants

- Retail Stores

- Health Clubs

- Day Care Facilities

- Car Washes

- Farmers Markets

- Boutiques

- Auto Repair Shops

- Convenience Stores

Manufacturing and Industrial

Whether you need to purchase a piece of highly specialized equipment, are expanding to a larger facility, or are looking to make energy efficiency improvements, we’re here to help you. We’ve been providing financing to manufacturing and industrial firms since 1982 on projects ranging from $200,000 to $20 million, such as:

- Recycling Facilities

- Food Manufacturing

- Steel Production

- Packaging Companies

- Commercial Printers

- Machine Shops

- Freight and Transport

- Wholesalers

How Would an SBA 504 Loan Benefit Me?

By and large, use of the 504 Loan Program provides a financing solution that can ease business owners’ expansion concerns. And, with recent program enhancements, the 504 is now able to help more businesses than ever before.

12 benefits that prove SBA 504 Loans were specifically designed to help businesses expand and prosper…

- Low down payments (10% in most cases)

- Low, fixed interest rate on the 504 portion

- Long loan terms – up to 25 years

- The ability to include furniture, fixtures and fees

- An option for refinancing commercial debt

- Payment stability

- Preservation of working capital

- Protection from balloon payments

- The ability to include leasehold improvements

- Up to $5 million for SBA portion of the loan, and no limit on the overall project size

- The option of using the 504 Loan Program multiple times to continue expansion

- The ability to keep your current bank/lender

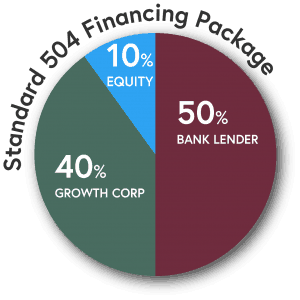

How does the 504 Loan Program Work?

The loan itself is a partnership between you, your CDC (such as Growth Corp), and a local bank. The breakdown typically looks like this:

- 50% of the project’s total cost will come from a conventional lender (your bank). You and your lender will determine the conditions of that loan, including the amount. This loan is the first mortgage.

- 40% of the project’s total cost will come from a CDC (Growth Corp) with a 10-year or 20-year fixed rate loan guaranteed by SBA. This loan is the second mortgage.

- The remaining 10% of the project’s total cost will come from you, the borrower. Certain types of facilities are classified as “single-purpose” facilities and may require additional equity, but most projects fall into the 50-40-10 split.

Since 1996, the 504 Loan Program has facilitated over $151 billion in total expansion financing.

Is My Project Type a Good Fit for an SBA 504 Loan?

To qualify for an SBA 504 loan, your intended use of the financing must be one of the following:

- Purchasing equipment or machinery

- Purchasing land or existing buildings

- Purchasing improvements (e.g. street grading, utilities, parking lots, etc.)

- Building new facilities

- Renovating, remodeling, or converting existing facilities

- Refinancing existing debt that’s being used to pay for fixed assets

Will Money for SBA Lending Continue to Be Available?

There is plenty of money available for lending. In fact, Congress has recently displayed significant effort in making SBA Loan Programs, including the 504 Loan Program, available to even more businesses. With higher loan limits and expanded eligibility standards, more businesses are now able to utilize the 504 than ever before.

Have more questions?

Check out our Frequently Asked Questions page.

Can Growth Corp Help Me Secure an SBA 504 Loan?

Yes! With one caveat…Growth Corp is only authorized to administer 504 Loans in Illinois and the surrounding area.

If you’re outside of the Midwest, you can find a Certified Development Company (CDC) using SBA’s CDC finder tool. We always recommend working with an ALP (Accredited Lender Program) CDC as they usually have preferred processing with the SBA.

Since the 504 is a partnership between a bank and CDC, you’ll also need to find a bank that’s willing to work on the bank portion of the loan too. Many national, regional, and community banks participate in the SBA 504 lending program and you can most likely stay with the lender you already use for your business banking.

In closing, virtually no loan is more sought-after than the SBA loan. Partially guaranteed by the government, SBA loans are long-term loans that can be used for practically any purpose. When it comes to rates and terms…again, it’s hard to find a more favorable loan option. Contact our team of qualified lenders, who are experts at helping small business owners get approved for SBA 504 loans that can help them compete, grow and succeed.